Basic Usage

The main function of the package is mich(), which takes

a vector or matrix of observations y and returns a

mich.fit object containing a variational approximation to

the posterior distribution of the change-points in the mean and/or

variance of y. The integer valued parameters

L, K, and J specify the

respective numbers of mean, variance, and joint mean and variance

change-points in y. In each of the examples below, we

sample a series with two changes in the mean and/or variance at times

101 and 201 and use mich() to

estimate and construct 95% credible sets around the locations of the

changes.

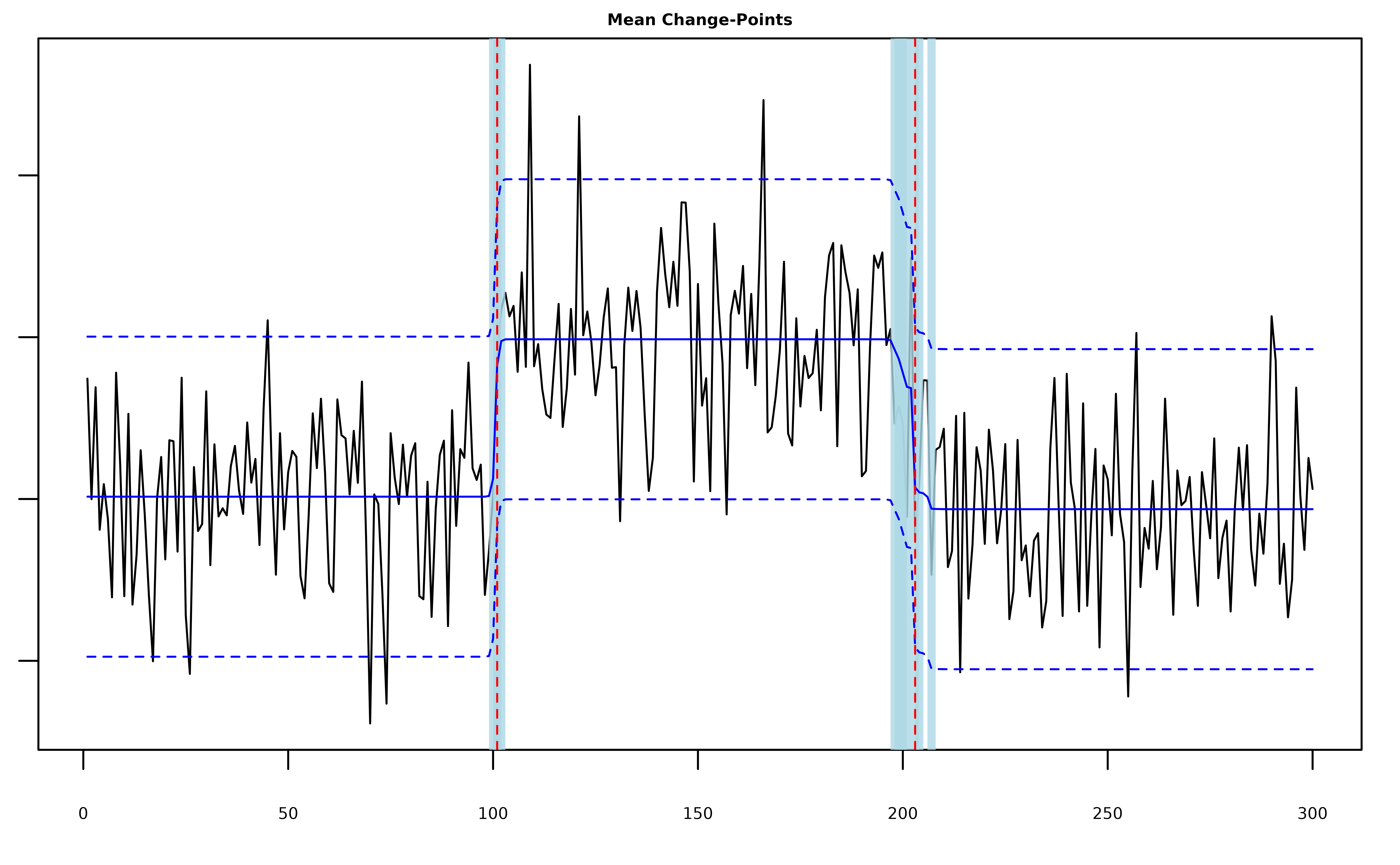

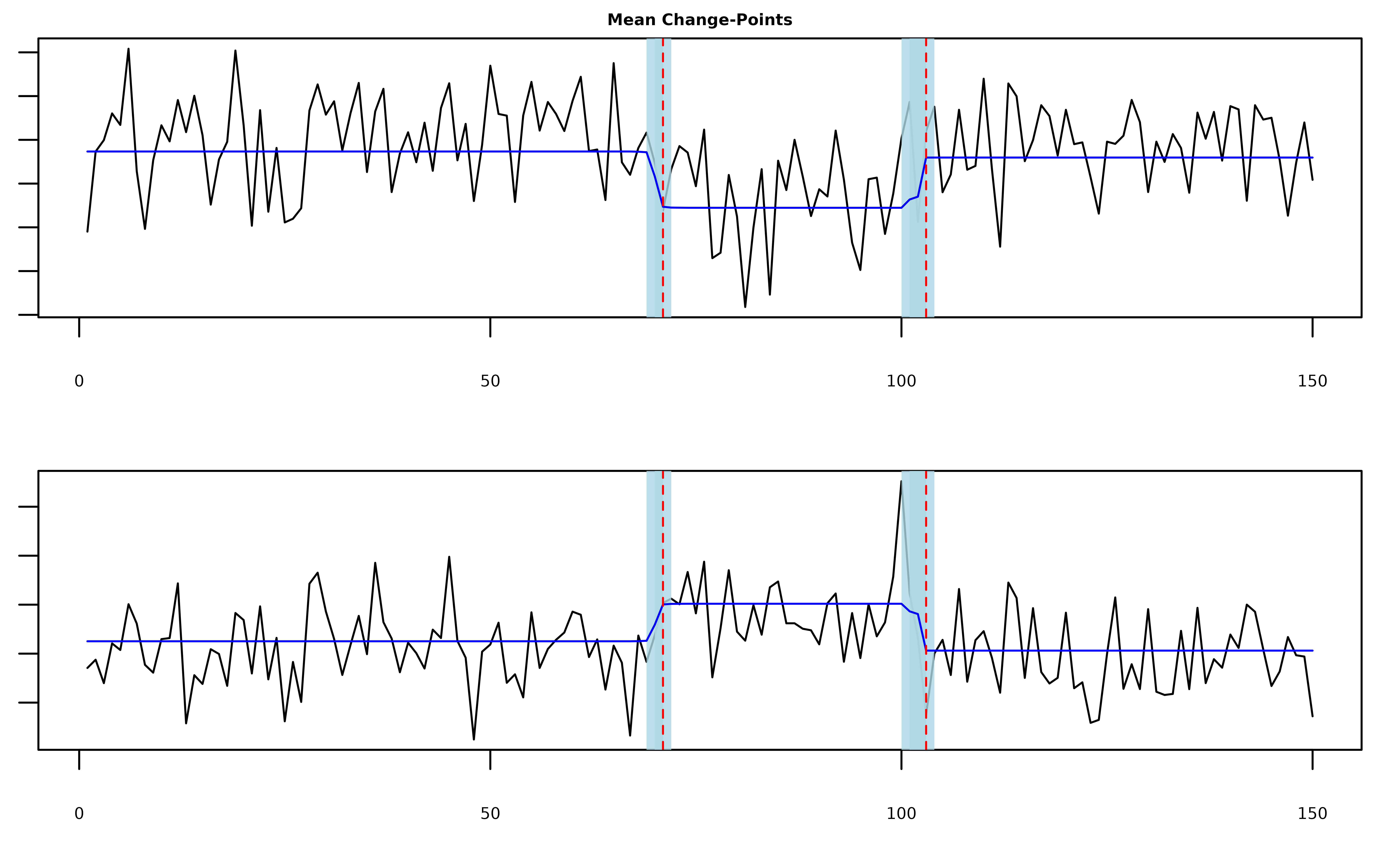

Mean Changes

# generate univariate data with two mean change-points

y = c(rnorm(100,0), rnorm(100,2), rnorm(100,0))

# fit two mean-scp components

fit = mich(y, L = 2)

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -242.324141949562; Converged: TRUE

#>

#> L = 2 Mean-SCP Component(s); 2 Detected Mean Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 101 100 102

#> 2 203 198 207The summary output shows us the ELBO for the fitted model as well as

the estimated locations of the changes and the lower and upper bounds of

the level-level credible sets around each change. Because

we called mich() with L > 0, the returned

mich.fit object contains a named list

mean_model that contains the posterior parameters for each

of the L components in the model. The most important

element is pi_bar, which is a T x L matrix of posterior

change-point location probabilities (for a detailed description of each

element of mean_model, type ?mich in the

console). We can use pi_bar along with the function

mich_sets() to construct change-point estimates and

credible sets.

# MAP estimates with 95% credible sets

mich_sets(fit$mean_model$pi_bar, level = 0.95)

#> $cp

#> [1] 101 203

#>

#> $sets

#> $sets[[1]]

#> [1] 100 101 102

#>

#> $sets[[2]]

#> [1] 198 199 200 201 203 204 207The plot() function is extended to the

mich.fit class and uses mich_sets() to plot

the returned MAP estimates as well as the estimated signal if

signal == TRUE and credible sets if cs == TRUE

(note that as in the plot below, these truly are sets, not

intervals).

plot(fit, cs = TRUE, level = 0.95, signal = TRUE)

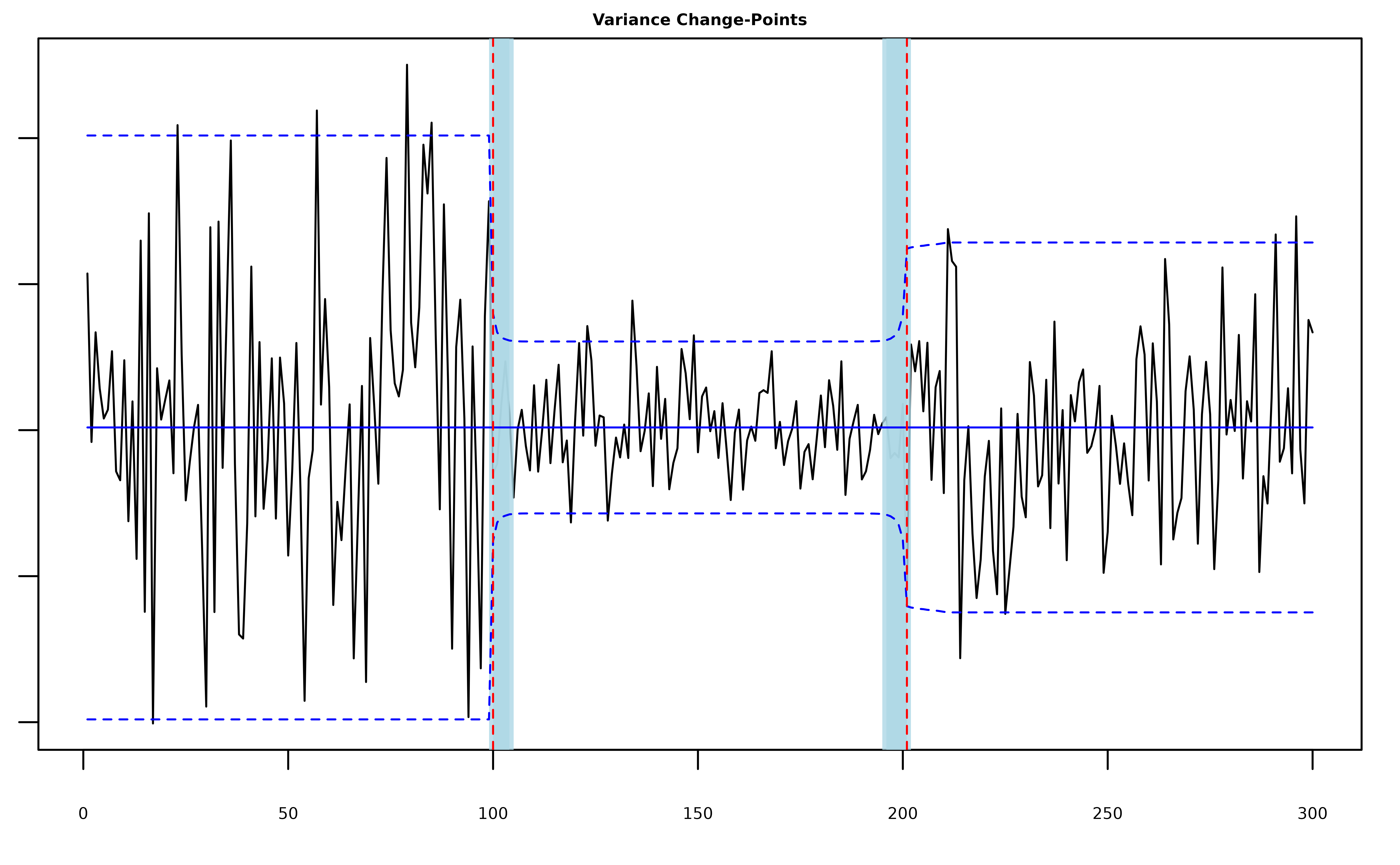

Variance Changes

# generate univariate data with two variance change-points

y = c(rnorm(100,0,10), rnorm(100,0,3), rnorm(100,0,6))

# fit two var-scp components

fit = mich(y, K = 2)

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -362.67485155576; Converged: TRUE

#>

#> K = 2 Var-SCP Component(s); 2 Detected Variance Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 100 100 104

#> 2 201 196 201The posterior quantities are now stored in

fit$var_model$pi_bar.

plot(fit, cs = TRUE, level = 0.95, signal = TRUE)

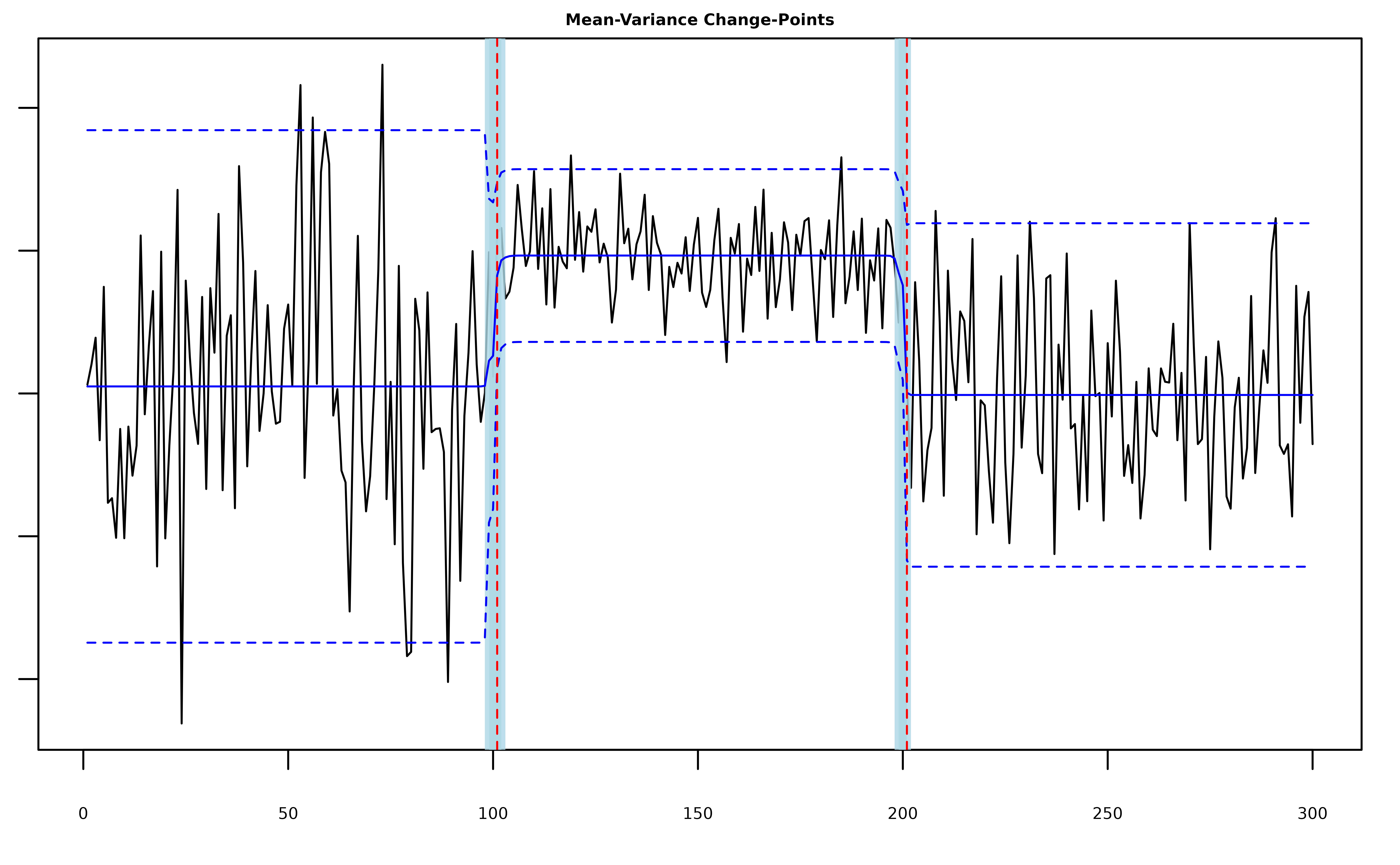

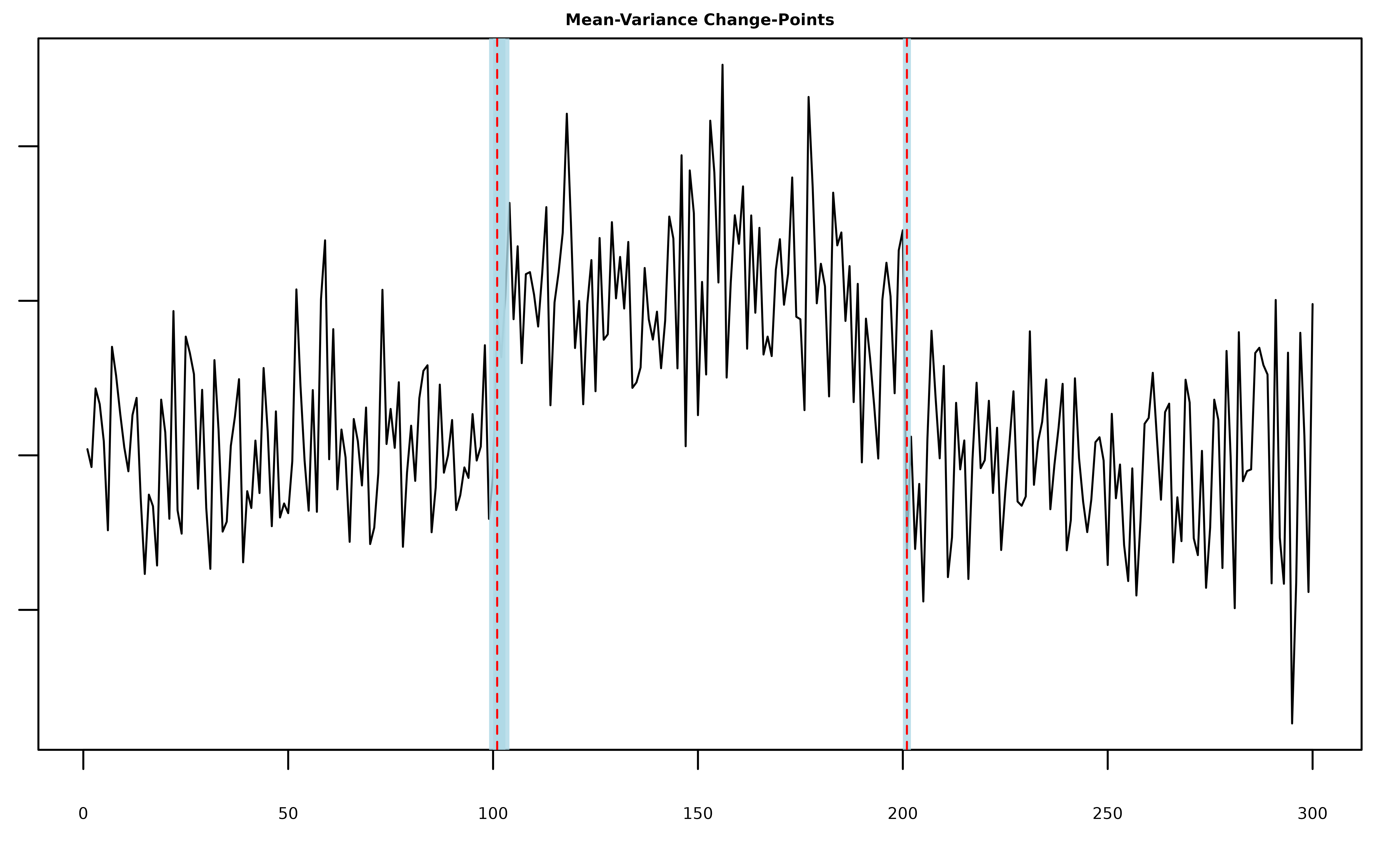

Mean-Variance Changes

# generate univariate data with two mean-variance change-points

y = c(rnorm(100,0,10), rnorm(100,10,3), rnorm(100,0,6))

# fit two meanvar-scp components

fit = mich(y, J = 2)

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -220.537132456086; Converged: TRUE

#>

#> J = 2 MeanVar-SCP Component(s); 2 Detected Mean-Variance Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 101 99 102

#> 2 201 199 201The posterior quantities are now stored in

fit$meanvar_model$pi_bar.

plot(fit, cs = TRUE, level = 0.95, signal = TRUE)

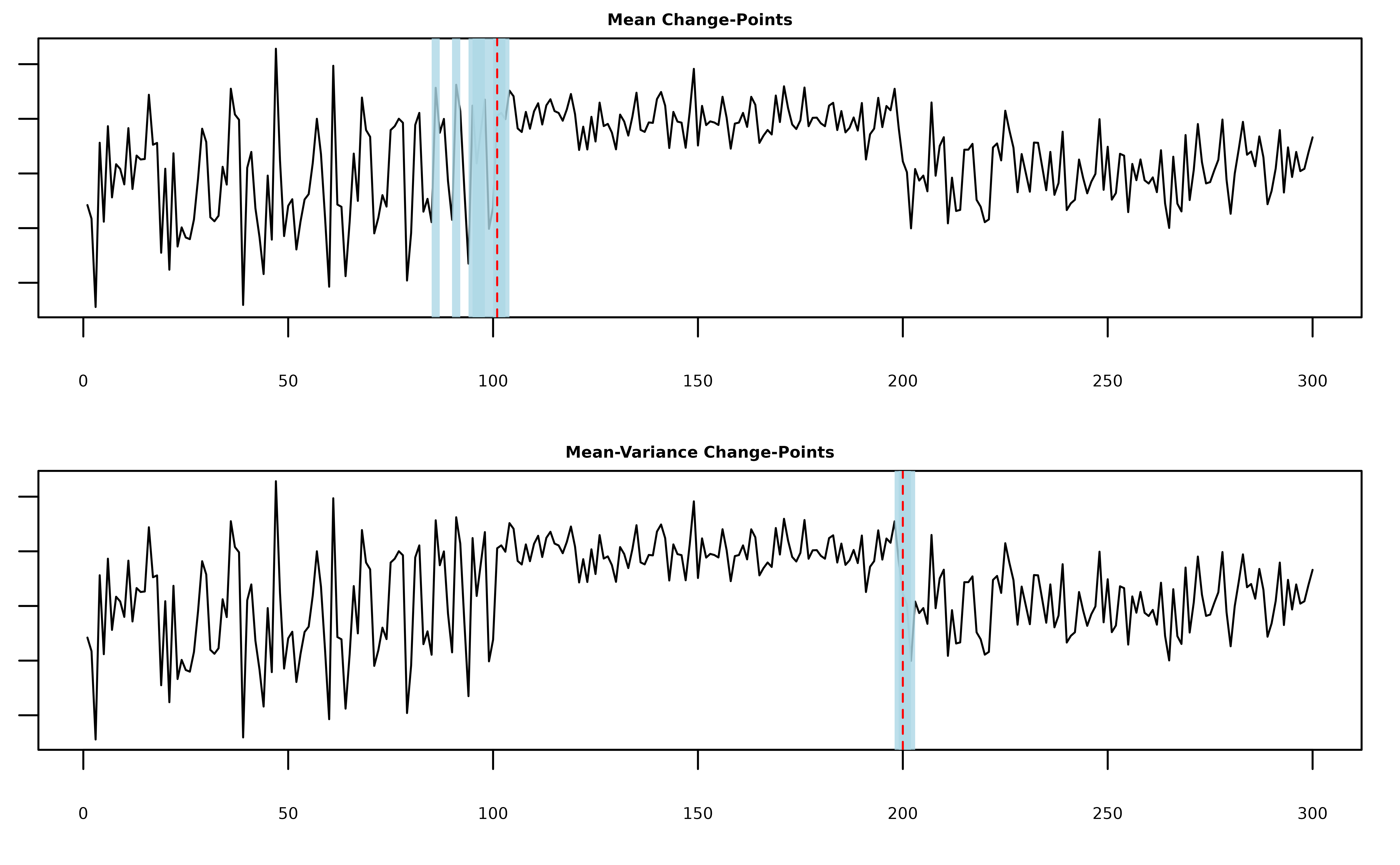

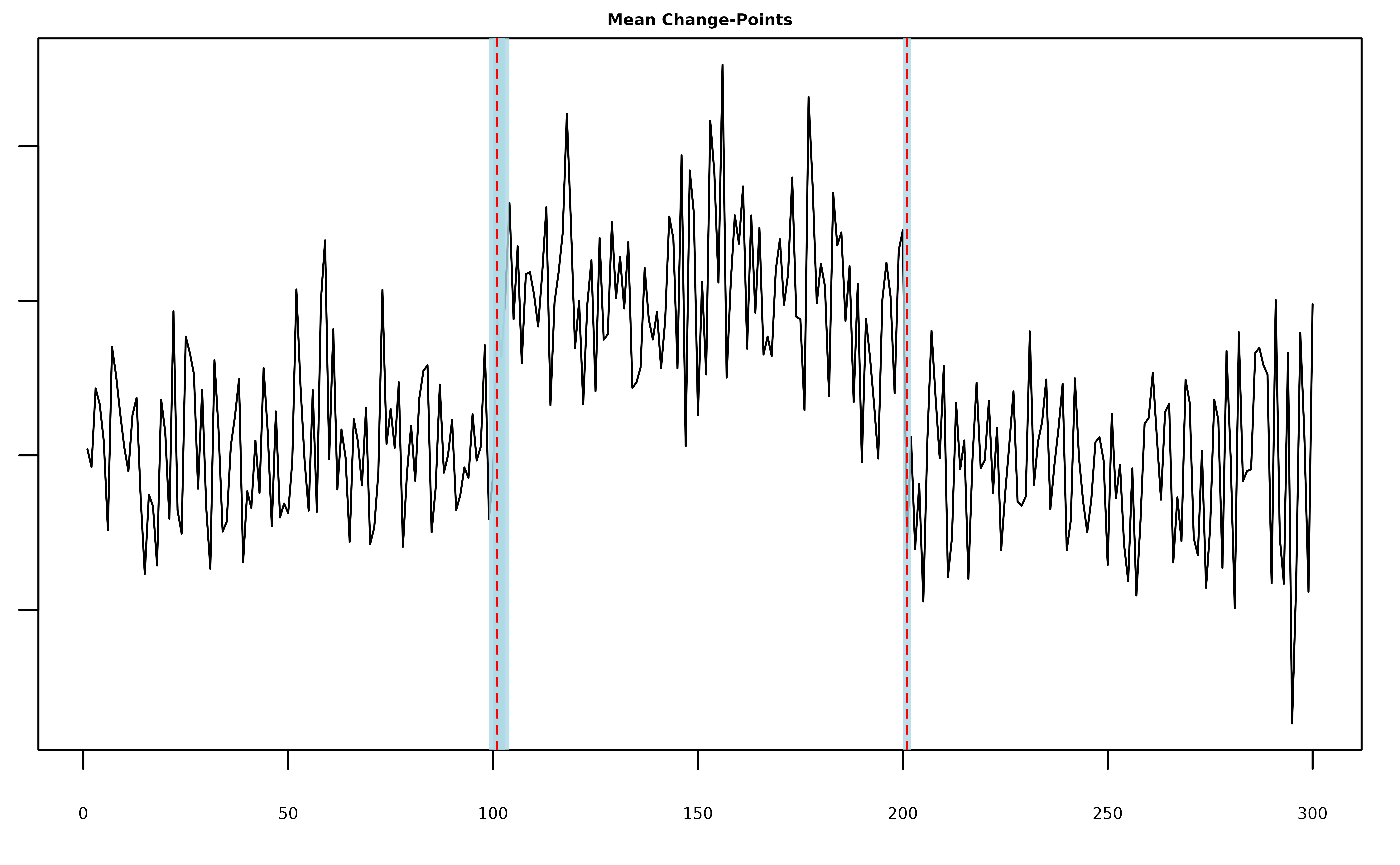

Multiple Change-Types

Note that by default L=K=J=0, so the call

mich(y) will fit the null model assuming no changes are

present in the mean or variance of y. It is also possible

to fit mich() with multiple kinds of changes, e.g. we could

rerun the last example with one of the changes misspecified as just a

mean change.

# generate univariate data with two mean-variance change-points

y = c(rnorm(100,0,10), rnorm(100,10,3), rnorm(100,0,6))

# fit one mean-scp component and meanvar-scp component

fit = mich(y, L=1, J = 1)

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -254.723737904751; Converged: TRUE

#>

#> L = 1 Mean-SCP Component(s); 1 Detected Mean Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 101 86 103

#>

#> J = 1 MeanVar-SCP Component(s); 1 Detected Mean-Variance Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 200 199 202We see that the model uses the mean-component to fit the first change and the mean-variance component to fit the second change.

plot(fit, cs = TRUE, level = 0.95)

Multivariate Mean Changes

In the case where y is a T x d matrix,

mich() can detect mean changes that are shared across all

or some of the columns. The columns of y do not need to be

independent and by default mich() will attempt to estimate

the precision matrix of the series (see the discussion of the

fit_scale parameter below). In the following example

y[,1] and y[,2] are positively correlated.

T <- 150

d <- 2

# covariance matrix

Sigma <- rbind(c(1, 0.7), c(0.7, 2))

Sigma_eigen <- eigen(Sigma)

e_vectors <- Sigma_eigen$vectors

e_values <- Sigma_eigen$values

Sigma_sd <- e_vectors %*% diag(sqrt(e_values)) %*% t(e_vectors)

# construct mean signal

mu <- c(-1, 2)

mu_t <- matrix(0, nrow = 70, ncol = d)

mu_t <- rbind(mu_t, t(sapply(1:30, function(i) mu)))

mu_t <- rbind(mu_t, matrix(0, nrow = 50, ncol = d))

# generate data

Z <- sapply(1:d, function(i) rnorm(T))

Y <- mu_t + Z %*% Sigma_sd

# fit two multivariate mean-scp components

fit = mich(Y, L = 2)

plot(fit, cs = TRUE, level = 0.95, signal = TRUE)

Selecting L, K, and J

In the previous section we treated the numbers of each kind of

change-point as known quantities, but more often than not we need to

estimate these parameters. One option is to set L,

K, and J equal to some large numbers that

upper bound each kind of change. For example if we think there are at

most five mean changes in the data then we can set

L = 5.

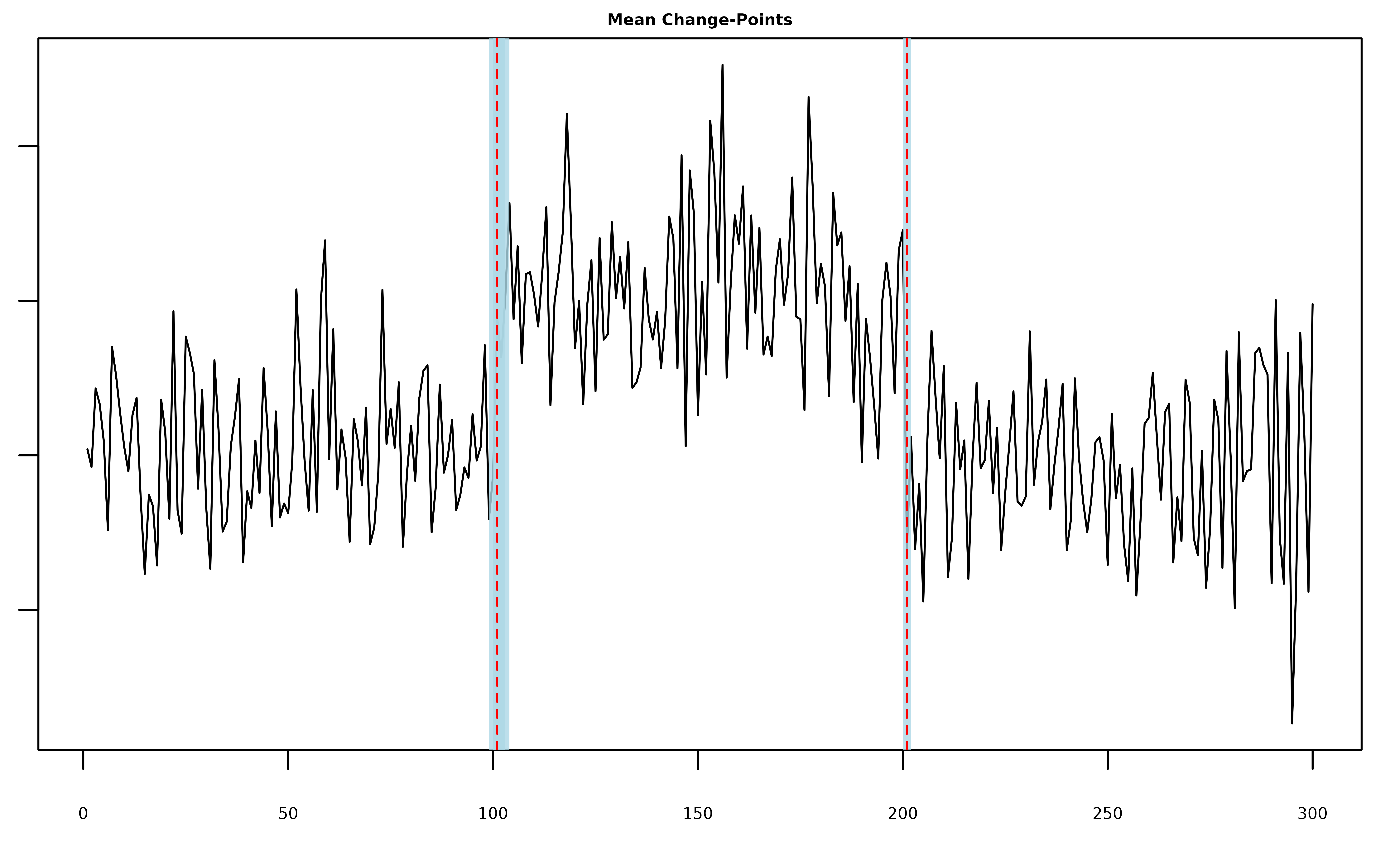

# generate univariate data with two mean change-points

y = c(rnorm(100,0), rnorm(100,2), rnorm(100,0))

# fit five mean-scp components

fit = mich(y, L = 5)

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -226.57173121568; Converged: TRUE

#>

#> L = 5 Mean-SCP Component(s); 2 Detected Mean Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 101 100 103

#> 2 201 201 201

plot(fit, cs = TRUE, level = 0.95)

Note that the model still only detected the two true change-points.

The plot below shows that this is because the extra three components we

included have very diffuse posterior distributions that do not satisfy

the detection criterion of having credible sets containing fewer than

log(T)^2 indices (see Corollary 1 of Berlind, Cappello, and Madrid

Padilla (2025)).

Auto-MICH

Alternatively, we can use the ELBO as an approximation to marginal

likelihood of the model and automatically select the L,

K, and J that maximizes the ELBO. This option

is implemented in mich() via the L_auto,

K_auto, and J_auto parameters. If

L_auto == TRUE, then mich() searches for the

number of mean changes between L and L_max

that maximize the EBLO.

# fit mich with L selected automatically

fit = mich(y, L_auto = TRUE, verbose = TRUE, restart = FALSE)

#> [1] "(L = 0, K = 0, J = 0): ELBO = -304.942450777234; Counter: 6"

#> [1] "(L = 1, K = 0, J = 0): ELBO = -298.331456279221; Counter: 6"

#> [1] "(L = 2, K = 0, J = 0): ELBO = -211.047722355175; Counter: 6"

#> [1] "(L = 3, K = 0, J = 0): ELBO = -215.885482079647; Counter: 6"

#> [1] "(L = 4, K = 0, J = 0): ELBO = -220.962514999129; Counter: 5"

#> [1] "(L = 5, K = 0, J = 0): ELBO = -226.200102703732; Counter: 4"

#> [1] "(L = 6, K = 0, J = 0): ELBO = -231.558781723112; Counter: 3"

#> [1] "(L = 7, K = 0, J = 0): ELBO = -237.01160903598; Counter: 2"

#> [1] "(L = 8, K = 0, J = 0): ELBO = -242.541140918896; Counter: 1"

#> [1] "(L = 9, K = 0, J = 0): ELBO = -248.136597702824; Counter: 0"

#> [1] "Merging. Merge Counter: 1"

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -211.048798898986; Converged: TRUE

#>

#> L = 2 Mean-SCP Component(s); 2 Detected Mean Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 101 100 103

#> 2 201 201 201Once again mich() is able to correctly identify the

mean-changes, but now setting L_auto == TRUE results in a

model with only two components.

plot(fit, cs = TRUE, level = 0.95)

Similarly, if K_auto == TRUE or

J_auto == TRUE then mich() searches for the

optimal number of variance and mean-variance components to include in

the model. It is possible to have some combination of

L_auto, K_auto, and/or J_auto set

equal to true, in which case mich() takes turns

incrementing L, K, and J and

moves in the direction that results in the largest increase in the

ELBO.

# fit mich with L selected automatically

fit = mich(y, L_auto = TRUE, J_auto = TRUE, verbose = TRUE, restart = FALSE)

#> [1] "(L = 0, K = 0, J = 0): ELBO = -304.942450777234"

#> [1] "(L = 0, K = 0, J = 1): ELBO = -290.56141335325"

#> [1] "(L = 1, K = 0, J = 0): ELBO = -298.331456279221"

#> [1] "(L = 0, K = 0, J = 2): ELBO = -226.747670431813"

#> [1] "(L = 1, K = 0, J = 1): ELBO = -308.614869844839"

#> [1] "(L = 0, K = 0, J = 3): ELBO = -235.207021249792"

#> [1] "(L = 1, K = 0, J = 2): ELBO = -232.203193790049"

#> [1] "(L = 1, K = 0, J = 3): ELBO = -247.407027549628"

#> [1] "(L = 2, K = 0, J = 2): ELBO = -232.674862962079"

#> [1] "(L = 2, K = 0, J = 3): ELBO = -247.141610997682"

#> [1] "(L = 3, K = 0, J = 2): ELBO = -238.433249627662"

#> [1] "(L = 3, K = 0, J = 3): ELBO = -250.526457976407"

#> [1] "(L = 4, K = 0, J = 2): ELBO = -243.104705526494"

#> [1] "(L = 4, K = 0, J = 3): ELBO = -257.781771835369"

#> [1] "(L = 5, K = 0, J = 2): ELBO = -248.914056107144"

#> [1] "(L = 5, K = 0, J = 3): ELBO = -264.495764094318"

#> [1] "(L = 6, K = 0, J = 2): ELBO = -254.768484151035"

summary(fit, level = 0.95)

#> Univariate MICH Model:

#>

#> ELBO: -226.747670431813; Converged: TRUE

#>

#> J = 2 MeanVar-SCP Component(s); 2 Detected Mean-Variance Change-Point(s):

#> change.points lower.0.95.credible.set upper.0.95.credible.set

#> 1 101 100 103

#> 2 201 201 201

plot(fit, cs = TRUE, level = 0.95)

Lastly, mich() accepts the integer valued parameter

increment, which determines how many components are added

to the model as mich() searches for the best

L, K, and/or J, and

restart, which causes mich() to refit the

model from a null parameterization once the ELBO stops increasing, which

can help the variational algorithm escape local minima.

Priors

Prior Change-Point Location Probabilities

The priors for the change-point locations are controlled by the

pi_l, pi_k, and pi_j parameters

(each corresponding the the prior locations of mean, variance, and mean

and variance changes). By default these parameters are set equal to

"weighted", in which case the functions

log_mean_prior(), log_var_prior(), and

log_meanvar_prior() are used to calculated weighted priors

that ensure diffuse posterior distributions in the absence of any

changes in the mean and/or variance of y (see Appendix C.2

of Berlind, Cappello, and

Madrid Padilla (2025) for a detailed discussion). Setting

pi_l, pi_k, or pi_j equal to

"uniform" will force mich() to use the uniform

prior rep(1/T, T) instead. The user can also provide their

own priors by setting pi_l, pi_k, or

pi_j equal to a vector pi such that

length(pi) == length(y) and sum(pi) == 1, in

which case pi will be used as the prior for all of the

model components. pi can also be a matrix of probabilities

so long as nrow(pi) == length(y),

all(colSums(pi) == 1) == TRUE, and if

pi_l = pi then ncol(pi) == L and so on for

pi_k and pi_j.

Precision, Shape, and Rate Parameters

Each of the prior precision, shape, and rate parameters in the model

is set equal to 0.001 by default. The user can change these

parameters by modifying omega_l, u_k, v_k, omega_j, u_j and

v_j, but the sensitivity analysis in Berlind, Cappello, and Madrid

Padilla (2025) indicates that as long as these values are small,

they do not meaningfully alter the output of mich().

Standardization

When standardize == TRUE, mich() will

center and rescale the data before running the main variational

algorithm. While this step can help improve performance, because the

location of the first change-point is unknown, it does not guarantee

that y will begin centered at zero or have unit variance.

Instead, mich() estimates and returns an intercept

mu_0 and initial precision lambda_0 by default

(when y is a matrix, the estimated variance-covariance

matrix is returned instead as Sigma). If y is

known to be centered at zero or have unit variance, than the estimation

of these parameters can be avoided by setting

fit_intecept == FALSE and/or

fit_scale == FALSE.

Additonal Parameters

Additional control parameters can be viewed by typing

?mich in the console. These include the convergence

criterion tol, a verbose parameter that will

prompt mich() to provide feedback as it fits the model, and

a reverse parameter that will make mich() fit

to y[T:1] in place of y which can occasionally

improve the model fit.